Japan in Transition ― Economy, Monetary Policy and Tokyo’s Role as Global Financial Center

※This article is based on a presentation by Hiroshi Nakaso, Chairman of FinCity.Tokyo, at the Gathering of Chief Representatives of foreign central banks in Japan held on November 28, 2025. Please note that some of the data and figures cited reflect the situation at the time of the presentation.

Introduction

Today, I want to share my views on the state of Japan’s economy and monetary policy and the role of Tokyo as a financial center in the evolving global economy and finance.

1 Japan’s Economy and Monetary Policy

Japan’s Economy

I joined the Daiwa Institute of Research and FinCity Tokyo after completing 40 years of public service at the Bank of Japan. In the early days of my career at the central bank in the 1980s, Japan was on the rise. “Japan as No.1”, the title of the book written by Ezra Vogel was frequently and proudly referred to. Japanese banks were often compared to the Invincible Armada. All these proved illusions and were gone when the bubble burst in the early 1990s.

And then Japan entered into what is today called the “Lost Three Decades.” As many as 200 financial institutions went bust in the Japanese Banking Crisis of the 1990s. Their credit intermediary function was so badly damaged that they were unable to play the key role of supporting Japan’s economic recovery. That put Japan under persistent deflationary pressure. The Bank of Japan became a lonely forerunner in that we had to invent all sorts of unconventional monetary policy measures to overcome the deflation.

Thirty years on, Japan is back. We now have a sound financial system to support the economy. Deflation is finally behind us. Joint efforts by both the public and-private sectors paved the way to the comeback. This was a painful process, but lessons were learned. That is why I believe not everything was lost in the “Lost Three Decades.”

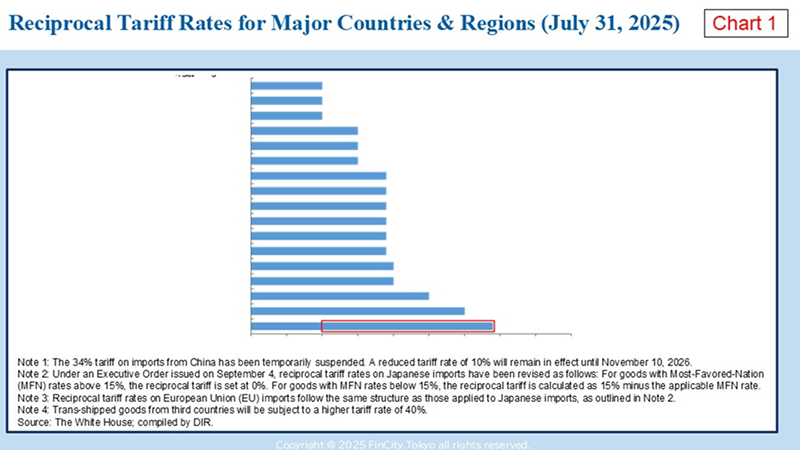

Currently, Japan faces heightened uncertainties arising from Trump 2.0 policies. Chart 1 compares reciprocal tariff rates for major economies. As we can see, the tariff rate for Japan, South Korea, and the EU is 15%, which is among the lowest.

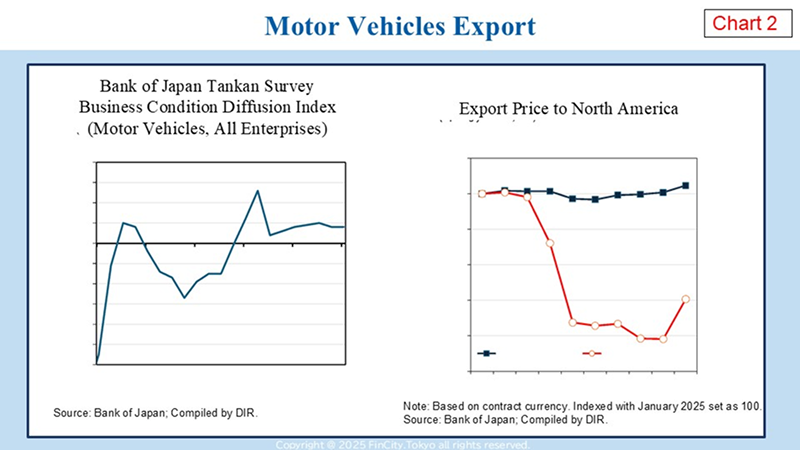

The focus of the economic impact of the US tariffs on Japan has been the automobile industry. In this respect, the BoJ’s latest TANKAN survey result, summarized in the chart on the left side of Chart 2, shows that business sentiment in the auto sector has in fact remained almost unchanged despite the US tariffs. The chart on the right shows that export prices of cars from Japan to the US declined by almost 20% since the beginning of the year.

This implies that Japanese auto manufacturers are squeezing their profit margins to contain the after-tariff sales prices with a view to maintaining a certain market share in the US. They have come through numerous trade conflicts against the US in the past. They survived the high exchange rate that once climbed to 80 yen against the dollar. Afterall, they are battle-hardened to dodge the bullet. It may be fair to say that the Japanese economy weathered the tariff storm and demonstrated resilience thus far.

Monetary Policy

The Bank of Japan in March 2024 embarked on monetary policy normalization by lifting all the unconventional policy measures that had been employed. After two policy rate hikes, however, the BoJ faces heightened uncertainties caused by Trump 2.0 policies. Against this backdrop, they have kept the policy rate on hold at 0.5% since January. They will resume policy rate hikes once they restore confidence in the economic and inflation trajectory to move in line with their projections.

On the inflation front, the BoJ is of the view that the risk of reverting to deflation cannot be ruled out. But I think there is in fact a risk also on the upside for the following three reasons.

a) High wage growth will likely continue into next year against the backdrop of the acute labor shortage.

b) Corporate pricing behavior has shifted in that they now find it easier to pass on higher costs caused by higher wages, supply chain disruptions and weaker currency, to final sales prices.

c) Inflation expectations in Japan, as both survey-based and market-based measurements are in a rising trend.

The third point needs to be paid more attention to. We know from empirical studies that inflation expectations in Japan are formulated in a backward looking (adaptive) manner more influenced by actually observed ongoing inflation rates.

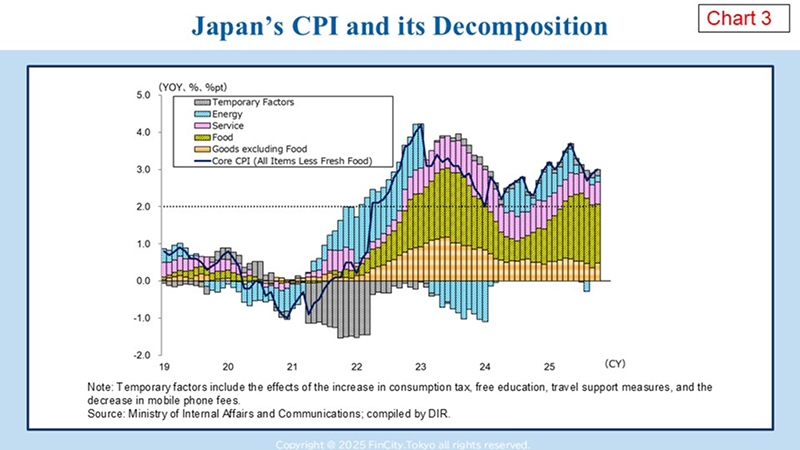

Inflation rates in Japan remain high by Japanese standards. The graph on Chart 3 shows core CPI inflation rates in the black solid line and contributing factors in bars in different colors. We have been facing CPI inflation rates exceeding the price-stability target of 2% for 43 months in a row. It is food inflation as the green bars show, exacerbated by the skyrocketing price of rice. This runs the risk of inflation expectations over-shooting. I think the monetary policy in Japan needs to be vigilant not to be left behind the curve.

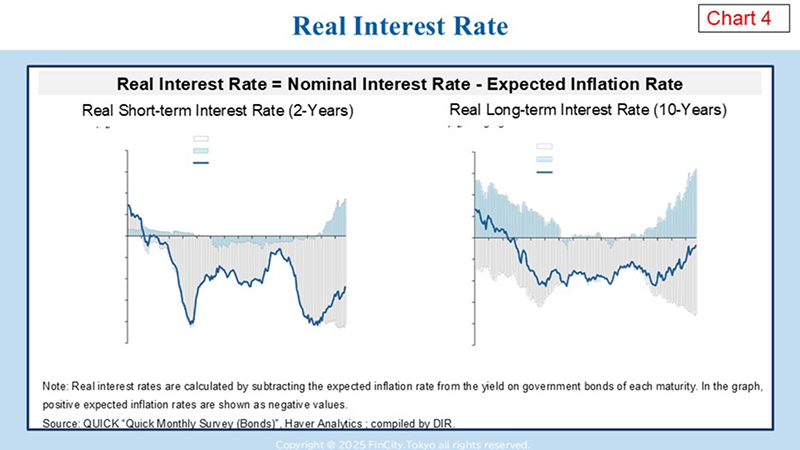

As shown in the graphs on Chart 4, real interest rates, which take account of inflation rates, remain negative both for short-and long-term interest rates. Therefore, another couple of rate hikes won’t materially change the accommodative monetary condition in Japan.

USD Liquidity Condition

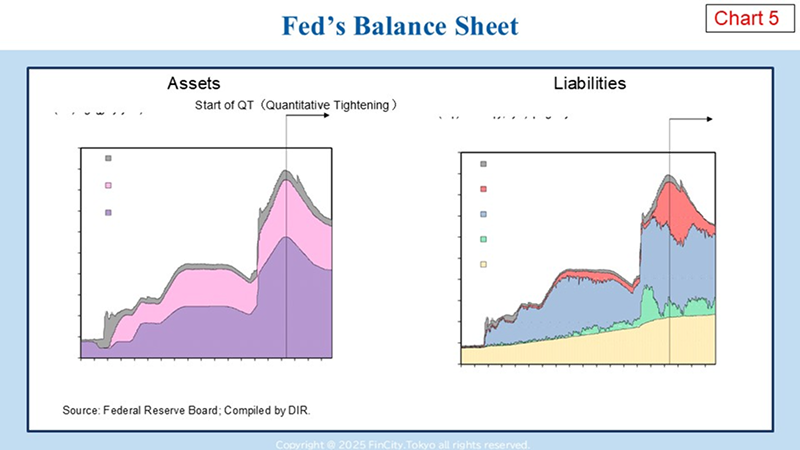

From a broader perspective, one thing to watch for the central banking community in the runup to the yearend is the USD liquidity condition as Fed terminates QT on December 1. As the Fed’s balance sheet shows on Chart 5, QT implies a reduction in US Treasury securities held by the Fed on the asset side and a corresponding decline on the liability side in Reverse Repo Agreements (in red color) and Deposits held by banks (or reserves in blue). The reserves represents the aggregate supply of liquidity to the interbank market, which as you can see has remained almost unchanged thus far.

Going forward, however, the widening US fiscal deficit is to be financed by more issuance of Treasury securities, the proceeds of which are placed with the US Treasury General Account at the Fed (in green color). Any further move will likely bite into the reserves.

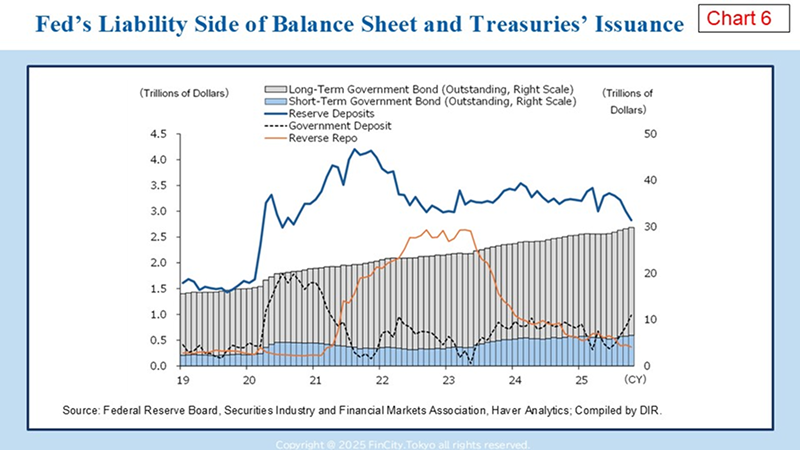

As shown in the graph on Chart 6, this has started to take place. Treasury General Account (in dotted line) is increasing against the backdrop of rising outstanding of Treasury Securities (shown in bars). This is accompanied by a corresponding decline in the Reserves (in blue solid line), since room for further reduction in the Reverse Repo (in yellow line) is limited. This means liquidity is drained from the market, which puts upward pressure on US money market rates.

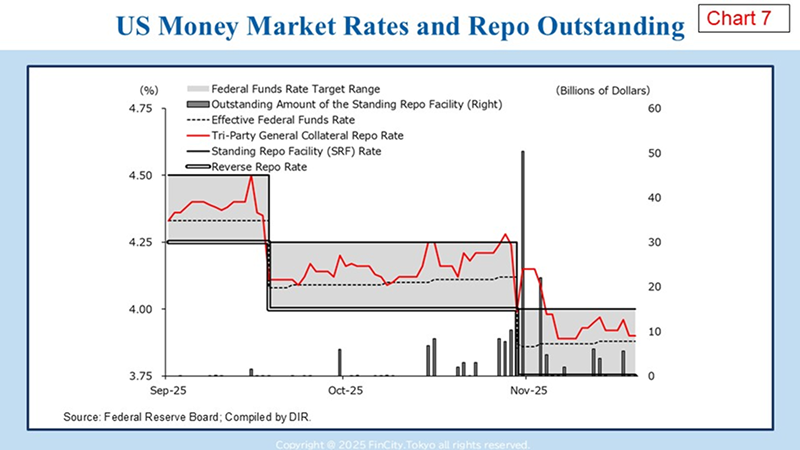

As a matter of fact, as you can see in the graph on Chart 7, there are instances recently when the repo rates (in red) overshoot the Fed Fund target range. The upward pressure is contained by more frequent use of the Fed’s Standing Repo Facility (SRF), as shown in bars, through which eligible financial institutions can borrow from the Fed. The SRF is meant to be a backstop but is often accompanied by notorious “stigma” on the part of borrowers, which dilutes the effectiveness particularly under market stress. In any case, this is the first yearend in many years with less ample USD liquidity. that deserves close monitoring.

2 Tokyo’s Role a Financial Center

Introducing FinCity.Tokyo and Our Achievement so far

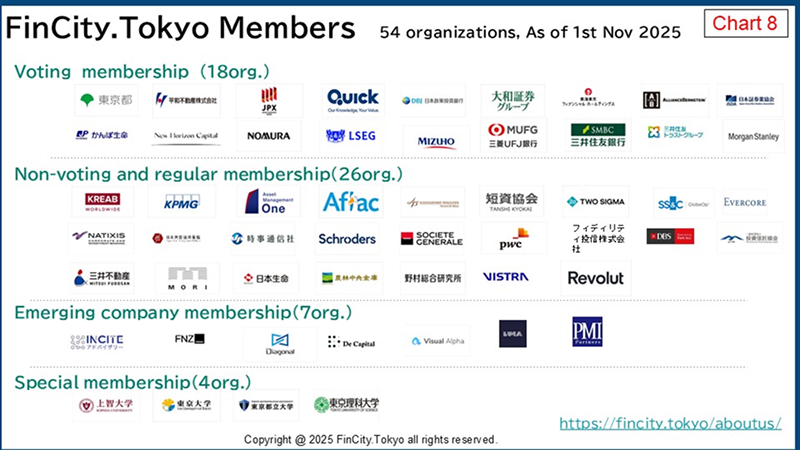

Next, I would like to explain about the FinCity Tokyo’s role to promote Tokyo as a financial center. FinCity.Tokyo was established in 2019 under the leadership of Tokyo Governor Yuriko Koike, who appointed me as Chairman. As shown on in Chart 8, our members comprise major financial institutions, the Tokyo Metropolitan Government, the JPX Group, and other key stakeholders. Starting with about 30 members, our organization has since grown to 54.

One of our key missions is to build a concentration of high-performing asset management firms and financial talents in Tokyo with a view to creating and adding a new investment channel to what has otherwise been a bank-centric intermediary system. The new channel is expected to direct Japan’s abundant capital into growth sectors.

This initiative bore fruit in several areas. First, FinCity Tokyo has been pushing the idea to invite both domestic and overseas asset managers to play a more active role in elevating investment returns with a particular focus on the so-called “emerging managers” which are typically small, independent, and active managers with high investment skills but with short track records. They have thus far been sidelined in Japan, where big asset management companies affiliated to parent banks and security houses were dominant.

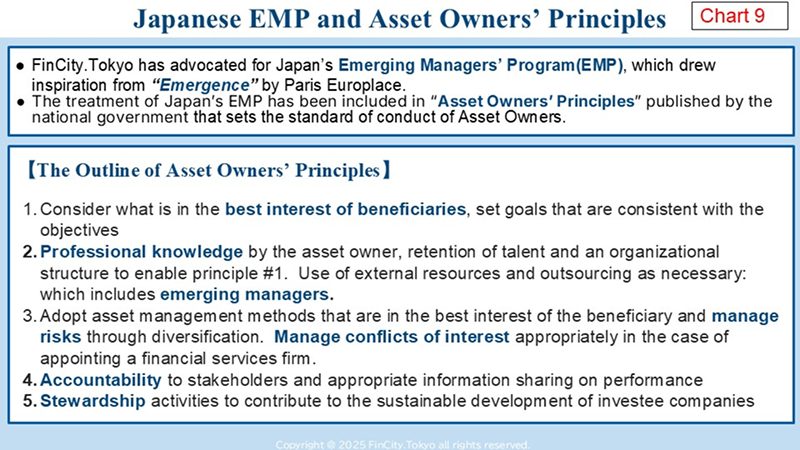

Our initiative was crystalized in the Government’s “Plan for Promoting Japan as a Leading Asset Management Center” compiled under the Kishida administration and subsequently developed into “Asset Owners Principles.” These government’s plans explicitly incorporated our proposal on the “Emerging

Asset Manager Promotion Program, or Japan EMP, aimed at providing greater business opportunities for emerging asset managers. Chart 9 outlines “Japan EMP” and “Asset Owners’ Principles”, which you might have a look at afterwards.

Second, there has been the growing recognition of the importance of our financial center initiative, attracting supporters from a wider base across Japan. What began as our independently organized annual event, “Tokyo Sustainable Finance Week,” is now a part of a broader nationwide annual financial event named “Japan Weeks,” led by the Financial Services Agency and hosted by various public and private stakeholders.

Third, Tokyo was designated “Asset Management Special Zone” in 2024 pursuant to the “Government’s Plan” alongside with Sapporo, Osaka, and Fukuoka. These cities are working together to attract new domestic and international players, draw in global investment capital, and create an ecosystem where funds are channeled to growth sectors such as startups and SMEs.

These efforts are yielding results. Since 2022, Tokyo attracted 21 financial firms including asset managers with their overall AuM totaling $170 billion.

Challenges and Opportunities for Tokyo

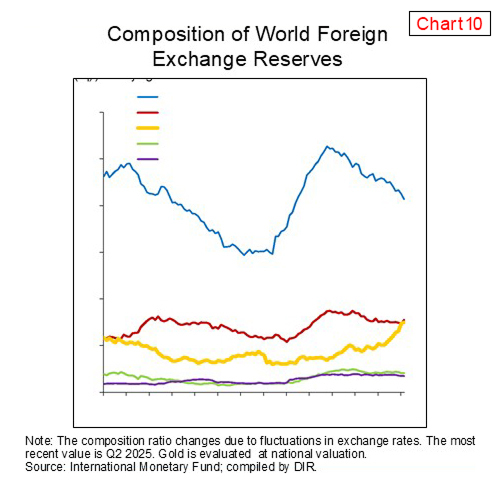

The shifting global financial landscape is working in favor of Tokyo’s role as a financial center. As shown in Chart 10, although the USD still accounts for the largest share of global foreign exchange reserves, that share has been on a downward trend since 2018. More recently, the weight of gold holdings has risen sharply, now catching up with that of the euro.

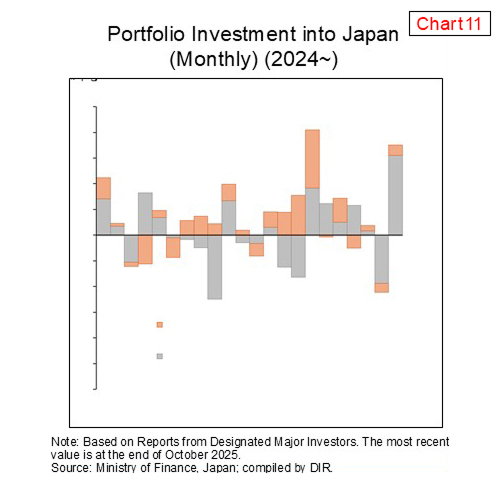

You might remember shortly after the shockwave triggered by the April 2 “Liberation Day”, there was a brief period when the value of dollar assets across the board plunged, as if a “Minsky Moment” had arrived, breaking the usual correlations among US Treasury securities, equity, and the dollar exchange rate. During this period, as shown in the right-hand side chart, Japan experienced a record high level of capital inflow totaling 8.2 trillion yen in April. The inflow trend seems to be continuing albeit with fluctuations.

Although I don’t think the USD supremacy as the key currency will be taken over any time soon, global investors’ portfolio diversification away from the USD into other currencies including the Japanese yen is likely to continue over time. There are more reasons why I believe Japan will continue to attract global capital, as outlined below.

a) The move from savings to investments continues as Japan is now back in the world with positive interest rates, offering more investment opportunities.

b) Stronger corporate governance spearheaded by the JPX that requires corporate management to be more conscious of capital costs and stock price, and

c) A lot of M&As including MBOs are in the pipeline as firms realign their business portfolios. The move will be compounded by the planned introduction of a stricter continuation criteria for listed companied set forth by the JPX. This is expected to leave many companies that are unable to meet the criteria to undergo M&As.

Fin City Tokyo’s mid-long strategy

Let me conclude by providing you with our mid-to long-term strategy, which is to position Tokyo as “Pioneer in Sustainable Finance in the Asia Pacific Region,” with a particular focus on Transition Finance. In other words, Tokyo aims to leverage finance to address the common challenge of climate change.

The hottest summer in history we experienced this year strongly argues in favor of the view that we should lose no time. The Japanese government remains committed to achieving carbon neutrality by 2050.

There is a broad agreement in the Japanese business community to incentivize not just “green” projects but also “amber” projects that can enable companies to realistically transition to achieve net zero goals. Given the diverse and multi-layered industrial base, not all companies can become green overnight. Therefore, I think it makes sense to move in steps in transition to decarbonization without moving the 2050 target backwards. This strategy is widely shared among economies in the Asia Pacific. Therefore, Tokyo wants to play a leading financial role in promoting smooth transition in the region.

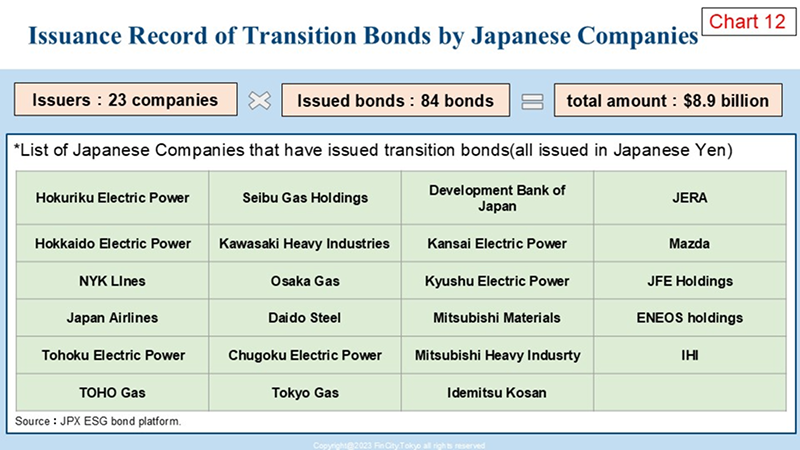

In this context, there are two initiatives to which we want to contribute more in collaboration with the private and public sectors. The first initiative is the promotion of issuance of Transition Bonds, which is one form of financial instrument specifically targeted at financing transition projects that contribute to reducing carbon emissions. As shown in the table on Chart 12, cumulative issuance of transition bonds issued by Japanese companies has exceeded $8.9 billion, steadily building expertise that Japan can offer to other economies facing climate challenges.

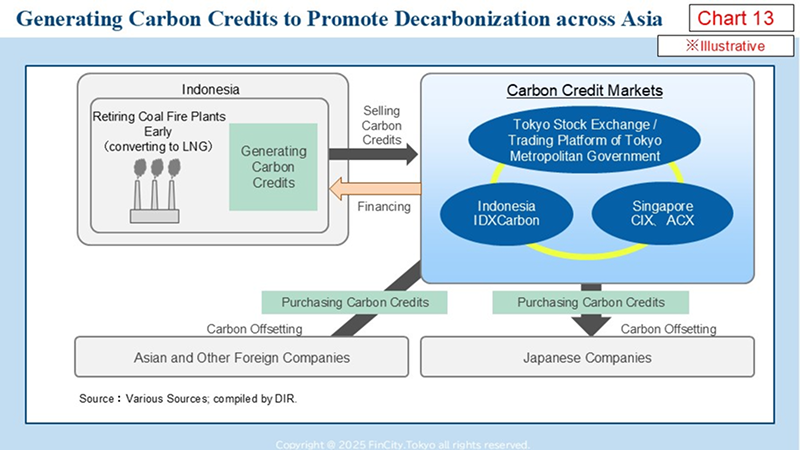

The second initiative is the creation of a network of “interoperable voluntary carbon credit markets” in the Asia-Pacific region. A conceptual example is illustrated on Chart 13. It shows a case in which an Indonesian electric power company reduced carbon emissions through the early retirement of a coal-fired power plant, converting it into a cleaner plant that burns LNG. In order to recover the huge cost for the new plant, a part of the reduced emissions can be sold as carbon credits to domestic as well as overseas markets like Tokyo and Singapore. Business companies in the region can purchase carbon credits to partially offset their carbon emissions. In this way, the economies across the region can collectively become green quicker than otherwise.

We are informed that the initiative is advancing to a new stage focusing on promoting alignment of economies in the region on common standards and practices to ensure integrity and interoperability of carbon credit trading. Likewise, exchange linkage may be expanded beyond the test-proven cross -exchange trade between ACX Singapore and IDX Carbon of Indonesia.

Conclusion

Tokyo’s defining characteristic is that it is an “onshore financial center” supported by Japan’s multi-layered industrial base with its extensive supply chains spanning across Asia. Therefore, Tokyo’s role is to meet the financing needs of the industries, thereby contributing to the sustained growth of economies in the Asia Pacific region. I think this Tokyo’s role is mutually complementary to those performed by other major financial centers in the region. Let me finish my presentation by reiterating that Tokyo remains committed to playing an integral role in these important initiatives. Thank you very much for your attention.